Most experienced real estate agents will identify a similar range of comparable sales for your property. The real difference isn't the data. It's how that data is interpreted.

A good property appraisal doesn't simply tell you what similar homes have sold for. It explains what those sales mean for your property, today's market conditions, and the strategy most likely to create buyer competition when your property launches. That's where better selling decisions begin.

That distinction sounds simple. In practice, it is the difference between a campaign that launches with momentum and one that spends six weeks finding the price the market was always going to pay.

This page explains what a property appraisal actually is, what a well-constructed one should contain, how it differs from a formal property valuation, and how to assess whether the figure you receive reflects current market evidence — or reflects what an agent thinks you want to hear.

If you are considering selling and want to understand what an appraisal should involve before you book one, this is where to start.

Comparable sales provide the evidence.

Experience turns that evidence into a selling strategy.

Before booking your appraisal, it is worth understanding that the report itself isn't the value. Understanding what the evidence means — and how it shapes your selling strategy — is what helps protect your final result.

Book Your Free Property Appraisal ↓What Is a Property Appraisal — and What Does It Actually Measure?

A property appraisal is an agent's assessment of what a property is likely to achieve in the current market if listed for sale. It is prepared by a licensed real estate agent, it is typically provided at no cost to the vendor, and it is the starting point for almost every residential sale in Australia.

What a property appraisal measures — when it is done correctly — is not the property's intrinsic worth, its replacement cost, or its council valuation. It measures one specific thing: what buyers who are searching in the current market are likely to pay for this property, in its current condition, competing against everything else available to them right now.

That is a narrower question than it sounds. It requires the agent to know four things specifically:

What comparable properties have sold for in the past 60 to 90 days — not what they were listed at, what they actually achieved at settlement

How long those properties took to sell — and what the ones that sat longer had in common with each other

What is currently listed in the same price bracket — and how many competing properties a buyer for this home is also looking at right now

What the current buyer pool looks like — whether there are active buyers in this price range, whether finance conditions are working in the vendor's favour, and whether demand is rising or contracting

An appraisal that answers all four of those questions with specific evidence is a genuinely useful document. An appraisal that arrives at a number without referencing any of them is not an appraisal. It is a figure designed to start a conversation — usually the conversation the agent wants to have, not the one the vendor needs.

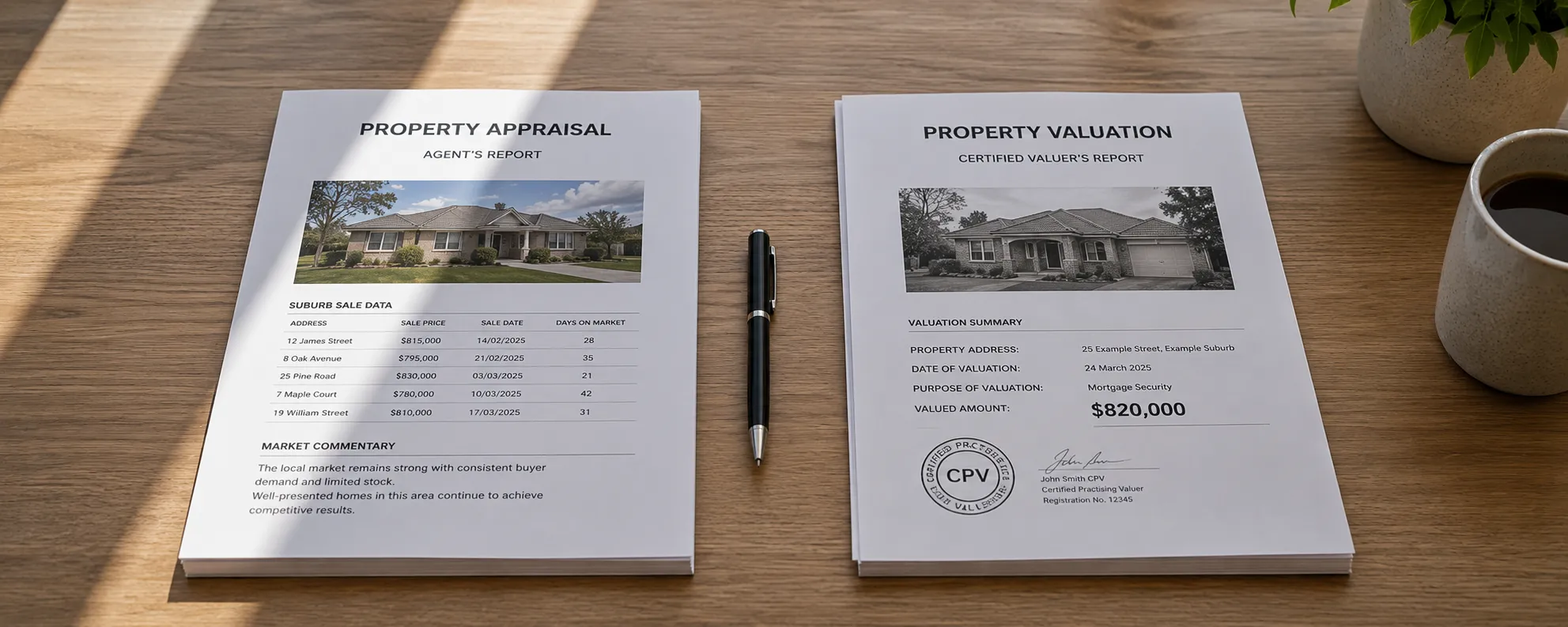

Property Appraisal vs Property Valuation — Understanding the Difference

The two terms are used interchangeably by vendors and even by some agents — but they describe fundamentally different documents prepared by different professionals under different legal frameworks.

- Prepared by a licensed real estate agent

- Opinion of likely market value based on comparable sales

- Not legally binding — no professional indemnity obligation

- Almost always provided free of charge

- Used for: making selling decisions

- Prepared by a licensed property valuer — a separate profession

- Legally binding opinion of value with professional indemnity

- Follows a defined methodology with registration requirements

- Typically costs $300 to $800

- Used for: mortgage lending, legal proceedings, estate administration, tax

Why the figures often differ

The figures in an appraisal and a formal valuation for the same property at the same time can differ significantly — sometimes by 10% or more. This is not necessarily because one is wrong. A formal valuation is typically conservative by design — it is prepared for a lender who needs to know the floor value of security, not the ceiling a motivated buyer might pay in a competitive campaign. An appraisal reflects what the market might pay with the right strategy. A valuation reflects what a lender can safely lend against.

How Much Does a Property Appraisal Cost?

Provided by a licensed real estate agent as standard practice across Australia

Prepared by a licensed valuer for mortgage, legal, or taxation purposes

In almost every case — nothing. Property appraisals in Australia are provided free of charge by licensed real estate agents. This is standard industry practice across every state and territory.

Understanding why they are free is useful context. An agent who conducts an appraisal is investing time in a potential client. The appraisal is the beginning of a business relationship — not a neutral service. The agent who provides the appraisal hopes to be engaged to sell the property. That is a legitimate commercial arrangement, and most vendors understand it implicitly.

What it means in practice is that every free appraisal exists within a competitive context. If multiple agents are appraising the same property, each one knows the vendor is likely to sign with whoever provides the most compelling case. For some agents, the most compelling case is the highest number. That incentive does not disappear simply because the appraisal is free.

A formal property valuation — prepared by a licensed valuer for mortgage, legal, or taxation purposes — is not free. Costs typically range from $300 to $800 for a standard residential property depending on location and purpose.

What Does a Good Property Appraisal Actually Contain?

Most vendors receive an appraisal as a number — sometimes a range, sometimes a single figure — delivered in a conversation or a brief document. What sits behind that number is rarely shown unless you ask for it.

The purpose isn't simply to produce a number. It's to help you understand how that number was reached and what it means for your selling strategy.

Most appraisal software today can produce attractive reports filled with comparable sales, maps, school locations and suburb information. Those reports are useful — but software doesn't decide which sales genuinely compare with your property, how buyers are likely to respond, or where your property should be positioned to generate competition. That's where professional judgement begins.

A well-constructed appraisal contains five things. Here is what each one looks like and why it matters:

The Framework

The Anatomy of a Good Property Appraisal

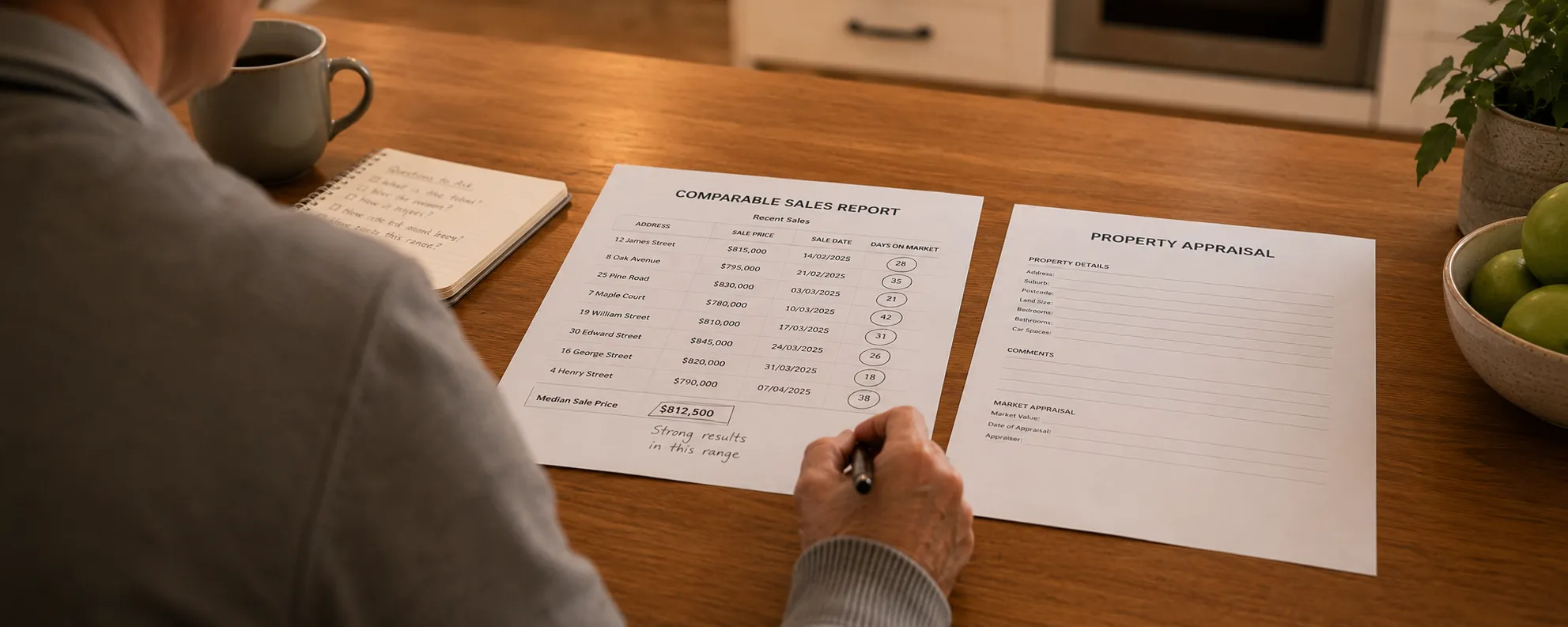

A Comparable Sales Analysis

A list of properties that have recently sold in the same suburb and price bracket that are genuinely comparable to yours — similar land size, floor area, bedroom and bathroom configuration, age, and condition. The key word is genuinely. A comparable sale is not simply a property in the same postcode. It is a property that a buyer considering yours would also have considered — and that a buyer chose to purchase instead of yours. The comparable sales should show the address, the sale date, the sale price, and the days on market. Any appraisal that does not include this information is asking you to trust a conclusion without showing you the evidence.

An Adjustment for Your Property's Specific Characteristics

No two properties are identical. A comparable sales analysis tells you what similar properties achieved. An accurate appraisal adjusts for the ways in which your property differs from those comparables — a larger land size, a more recently renovated kitchen, a corner position, a better or worse street. Those adjustments should be explained, not assumed. If an agent cannot tell you specifically why your property is worth more or less than a comparable sale, they have not done the analysis.

A Current Market Context Assessment

What is happening in your price bracket right now? How many competing listings are active? What is the average days on market for properties like yours? Is buyer demand increasing, stable, or contracting? These conditions affect what a correctly priced property will achieve — and they change month to month. An appraisal that does not account for current conditions is working from a snapshot that may already be outdated.

A Recommended Price Position

Not just what the property is worth — but where it should be listed to generate the maximum buyer interest during the Freshness Window. Those are related but not identical questions. A property worth $720,000 might be best positioned at $699,000 to attract buyers searching in the $650,000 to $700,000 range — producing more competition and a stronger final outcome than launching at $720,000 and waiting for the one buyer who will pay it. To see a worked property appraisal example showing exactly how comparable sales are analysed and a price position is constructed, the Pricing Framework page walks through the full methodology step by step.

An Honest Assessment of the Risks

What could work against this campaign? Is the property in a price bracket that currently has elevated competing stock? Is the timing working against it? Are there presentation issues that need to be addressed before launch? A good appraisal surfaces these questions rather than setting them aside to avoid an uncomfortable conversation. An agent who tells you only what you want to hear in the appraisal will tell you only what you want to hear throughout the campaign — and that pattern is most costly when the market gives you feedback you did not expect.

If the appraisal you receive contains all five of those things, it is an appraisal worth acting on. If it contains only a number and a confident assertion, it is a starting point for a conversation — not the conversation itself.

How to Get a Property Appraisal — and What to Ask Before You Book

Getting a property appraisal in Australia is straightforward — contact a licensed real estate agent and request one. Most agents will conduct a walkthrough of the property and provide their assessment within a few days. The process typically takes 30 to 60 minutes for the inspection itself.

What is less straightforward is knowing how to assess whether the appraisal you receive is worth acting on. These five questions, asked before or during the appraisal, will tell you quickly whether the agent in front of you is working from evidence or assertion:

The most important question. An agent who can produce a specific list of comparable sales — addresses, sale prices, sale dates, days on market — is working from evidence. An agent who refers to market trends or buyer sentiment without producing specific sales is working from assertion.

This question reveals whether the agent understands the cost of overpricing — and whether they are willing to discuss it honestly. An agent who deflects this question is not yet giving you the information you need.

An agent who knows this figure precisely — and can explain what it means for your campaign — has a current, granular understanding of your market. An agent who approximates or guesses does not. But understanding days on market requires one further distinction — see the section below.

Supply conditions in your specific price range affect how much attention your property will attract. If 15 properties are competing for the same buyers, that is materially different from entering a market with 5. An agent who knows this number is tracking your market actively.

An agent with real market knowledge will not wait until week four to have this conversation — they will already know, before the campaign launches, what the realistic timeframe looks like for your property in your price bracket. A good agent should be able to pull up the number of properties sold in your price bracket over the last one to three months and calculate a realistic days on market expectation from that data. An agent who tells you to wait for the right buyer without showing you that data is hoping rather than planning.

These questions take five minutes. The answers tell you more about an agent's market knowledge than any sales brochure or testimonial will.

Understanding Days on Market — What It Actually Tells You

Days on market is one of the most useful signals in any property campaign — but it is not a simple number. Properties that sit beyond the average days on market in any given suburb almost always fall into one of three categories. Understanding which category your property falls into before launch — not after four weeks on market — is what separates an agent running an informed campaign from one managing expectations downward after the fact.

The most common reason properties sit. A price set above where comparable sales are settling means buyers pass without offering. Avoidable with an evidence-based appraisal and an honest agent.

Larger or more expensive properties have structurally smaller buyer pools. A $1.2M home in a suburb with median sales of $750k will naturally take longer — not because it is overpriced, but because fewer buyers can purchase at that level.

Regional and rural markets have structurally smaller buyer pools regardless of price point. The average days on market in a country town is longer than in a suburban market — not because properties are overpriced, but because fewer buyers are looking at any given time.

An agent who can show you the sales volume data for your price bracket over the last one to three months — and calculate from that data what a realistic days on market expectation looks like — is an agent who has done the work. That analysis is what every appraisal should include, and what every vendor should ask for before launch.

The goal is not to know whether your campaign will take two weeks or eight. The goal is to enter the market with an honest expectation — so that if the first two weeks do not produce offers, you are acting from a plan rather than reacting from panic.

Why the Highest Appraisal Is Rarely the Most Accurate

The pattern is consistent enough across Australian residential markets that it has a name: the Appraisal Trap.

How the Appraisal Trap unfolds

A vendor invites two or three agents to appraise their property. One quotes $690,000. Another quotes $750,000. The vendor signs with the agent who quoted $750,000 — because the higher number feels like validation, like evidence that this agent understands the property's true worth.

Six weeks later the campaign has produced no offers at the listed price. The agent suggests a price reduction. The vendor agrees. The property sells for $705,000 — a price that an honest appraisal and a well-priced launch would have produced in the first two weeks, without the accumulated days on market that now sit publicly against the listing.

The vendor paid a higher commission rate, lost the momentum of the Freshness Window when buyer attention was at its peak, and achieved the same outcome they would have achieved from a correctly priced launch. The only winner in this sequence is the agent who won the listing.

This is not a rare occurrence. It is structural — a predictable consequence of an industry where agents compete for listings by quoting numbers that vendors want to hear.

Third-Party Validation

In March 2023, an ABC Four Corners investigation examined exactly these pricing practices within the real estate industry. The segment discussing over-quoting and conditioning appears from approximately 28 minutes and 20 seconds into the program.

The way to protect yourself: ask to see the comparable sales used to support the number. Specific properties, sale prices, dates — evidence you can verify yourself. A genuine appraisal comes with that. An inflated one comes with confidence and a promising figure. That is the difference.

Read the full Appraisal Trap guide — including the ABC Four Corners investigation →The question that protects you

"Show me the comparable sales in the last 90 days that support your appraisal — and tell me what happened to the properties in that data set that were priced above where they eventually sold."

An agent who can answer that with specific evidence is an agent whose number reflects the market. An agent who responds with generalisations, market sentiment, or enthusiasm about buyer demand without reference to actual comparable sales has given you a quote, not an appraisal.

Free Property Appraisal — What to Expect and What It Covers

A free property appraisal from a licensed agent typically follows a consistent process, though the quality of what is produced varies significantly between agents. Here is what a well-run appraisal looks like from inspection through to delivery:

Before entering the property, a thorough agent assesses the street appeal — what a buyer sees before they get out of the car. Kerb appeal forms the first impression in every listing photograph and at every open home. A property that presents poorly from the street is already working against itself before a buyer walks through the door.

The agent assesses the property against the comparable sales they have already reviewed. Land size, floor area, number of bedrooms and bathrooms, condition of key areas — kitchen, bathrooms, flooring — outdoor areas, and any features or defects that would influence a buyer's decision. The walkthrough typically takes 30 to 60 minutes.

After the walkthrough, the agent reviews recent comparable sales in the suburb and price bracket — adjusting for the specific characteristics of your property. This is where the evidence-based price position is constructed. Ask to see the comparable sales list. A well-prepared agent will have it ready before they arrive.

The agent presents their recommended price position — ideally a range rather than a single figure, with the lower end representing a realistic expectation and the upper end representing what a well-executed campaign in favourable conditions might achieve. If you receive a number without the supporting evidence, ask for it before you leave the conversation.

What a free appraisal does not cover

A free property appraisal does not constitute a formal valuation. It cannot be used for mortgage lending, legal proceedings, or taxation purposes. It is an agent's professional opinion of likely sale price — useful for making selling decisions, not for legal or financial obligations that require a certified valuer's report.

Andrew's Observation

The best appraisals don't simply provide evidence. They help homeowners understand what that evidence means so they can make confident decisions before their property ever reaches the market.

A vendor who receives a $750,000 appraisal and a $690,000 appraisal for the same property faces a real choice — and the natural instinct is to trust the higher number. It feels like the agent who quoted more believes in the property more. In most cases, that instinct is wrong.

The agent who quoted $750,000 may have done so because they know vendors are more likely to sign with the highest number. The agent who quoted $690,000 may have done so because they looked at the last twelve sales of comparable properties in the suburb and every one of them settled between $670,000 and $710,000.

One of those numbers is optimism. The other is evidence. They look identical until the campaign begins — and by the time the difference becomes visible, the Freshness Window has already closed.

What I have observed consistently in this market is that the vendors who achieve the strongest results are not the ones who received the highest appraisal. They are the ones who received an appraisal they understood — one that showed them the comparables, explained the adjustments, identified the risks, and gave them a price position that generated genuine competition during the first two weeks of the campaign.

A number without evidence is not an appraisal. It is the beginning of a negotiation — and not the negotiation between you and the buyer. The negotiation between you and the agent about what the market will actually pay.

One further observation worth stating clearly: the timeline for results must also be understood from the beginning — and it is not the same for every property. The Freshness Window applies universally, but what happens within it varies by price bracket. A well-priced family home in a suburb with strong buyer demand may attract offers in the first two weeks as a matter of course. A more expensive property — one that sits above the suburb median and requires a buyer with a larger deposit, stronger borrowing capacity, or a specific lifestyle need — will almost always take longer to find that buyer, even when the campaign is executing perfectly. That is not a failure of the campaign. It is the mathematics of a smaller buyer pool. An honest appraisal sets this expectation upfront — so that when week three arrives without an offer on a premium property, the vendor is acting from a plan, not reacting from anxiety. The agent who tells every vendor the same timeline regardless of price point is not giving advice. They are managing the conversation.

— Andrew McKiggan, Gawler East Real Estate RLA 248695

Frequently Asked Questions — Property Appraisal

A property appraisal is a licensed real estate agent's assessment of what a property is likely to achieve in the current market if listed for sale. It is based on comparable recent sales and current market conditions. It is an opinion of likely sale price — not a legally binding valuation. In Australia, property appraisals are almost always provided free of charge by agents as part of their business development process.

A property appraisal is prepared by a licensed real estate agent and reflects likely sale price in the current market. A property valuation is prepared by a licensed valuer — a separate profession — and is a legally binding document prepared for a specific purpose such as mortgage lending, estate administration, or legal proceedings. They serve different purposes and are prepared by different professionals. The full comparison is at the Property Appraisal vs Valuation guide.

A property appraisal from a licensed real estate agent is free in almost every case. A formal property valuation from a licensed valuer typically costs between $300 and $800 depending on the property and purpose.

This depends entirely on how the appraisal was constructed. An appraisal built from specific comparable sales data — recent sales of genuinely similar properties in the same suburb, adjusted for the differences between those properties and yours — is a reliable guide to likely sale price. An appraisal arrived at without reference to specific comparable sales is unreliable regardless of the confidence with which it is delivered. Ask every agent to show you the comparable sales that support their number.

Yes — a property appraisal carries no obligation to list. Most agents provide appraisals to vendors who are considering selling, planning ahead, or simply wanting to understand their current equity position. There is no requirement to proceed with a sale after receiving an appraisal.

The inspection itself typically takes 30 to 60 minutes. The agent will then review comparable sales data and provide their assessment — usually within a few days of the inspection, though some agents provide an initial indication at the end of the walkthrough.

Compare it against recent comparable sales in your suburb. If the appraisal figure is materially higher than what similar properties have recently achieved — and the agent cannot produce specific sales evidence that supports the difference — the appraisal is likely optimistic. The When a Property Appraisal Is Wrong guide covers the specific signals to watch for.

Yes — getting two or three appraisals from different agents gives you a basis for comparison and helps identify whether any one figure is significantly out of step with the others. When comparing appraisals, compare the evidence behind each number — the comparable sales used — not just the number itself. The highest figure is not automatically the most accurate.

Book Your Free Property Appraisal

Before booking your appraisal, it is worth understanding that the report itself isn't the value. Most experienced agents working from current market evidence will identify a similar range of comparable sales. What differs is how those sales are interpreted — and the strategy built from them.

Whether you eventually choose me or another agent, my hope is that this page helps you ask better questions, understand the information presented to you, and make a decision you'll feel confident about long after your property is sold.

Your appraisal won't simply provide a price range. Andrew will explain how comparable sales, current competition, buyer behaviour and today's market conditions combine to determine where your property is likely to sit — and why. No inflated number to win your listing, no pressure to sign before you are ready. Just an honest interpretation of the market and a clear explanation of the strategy most likely to protect your final result.

If you'd like to see how comparable sales, buyer psychology, current competition and market interpretation come together to determine your property's likely selling range, the Property Pricing Framework walks through the entire process step by step.

Choose a time that suits you using the booking button below, or complete the enquiry form and Andrew will be in touch personally.

Book instantly — choose your preferred time

No obligation. No pressure. Just a clear, honest assessment of what your property could achieve in today's market.

Local Perspective — Property Appraisals in Gawler and the Northern Adelaide Corridor

Andrew McKiggan is the principal and sole licensed agent of Gawler East Real Estate (RLA 248695), an independent residential agency based at 1 Lewis Ave, Gawler East SA 5118. Andrew provides free property appraisals across the Gawler district and northern Adelaide corridor — built from current comparable sales data, adjusted for the specific characteristics of each property, and delivered with an honest assessment of current market conditions and competing stock.

The appraisal principles outlined on this page apply across Australia, but the Gawler district has specific market characteristics worth understanding. The buyer pool here is driven substantially by affordability — buyers purchasing at or near the limit of their borrowing capacity, often relocating from more expensive inner suburbs. That profile makes price positioning particularly important. A property priced even marginally above where comparable sales are settling faces a more resistant buyer pool than equivalent properties in higher-price brackets.

Days on market accumulate quickly and publicly in this market. A property listed for 45 days without selling is not seen as patient by buyers — it is seen as overpriced. The Freshness Window is as short as anywhere in Adelaide, and the consequences of entering incorrectly priced are as real here as in any competitive metropolitan market.

For premium properties — those sitting above the suburb median — the timeline expectation must be set honestly from the beginning. A correctly priced premium property in Gawler may still take six to ten weeks to find the right buyer. That is not a campaign failure. It is the mathematics of a structurally smaller buyer pool at that price point, and an agent who does not explain this upfront is not giving you the information you need to make good decisions during the campaign.

If you are considering selling in Gawler or the surrounding suburbs — Hewett, Willaston, Evanston, Angle Vale, Munno Para — and want an appraisal built from current comparable sales rather than an optimistic figure designed to win your listing, the next step is a conversation.

If you are ready to speak with one of the real estate agents Gawler vendors trust for an honest, evidence-based appraisal and a straightforward commission structure, contact Andrew directly.

A property appraisal is the first decision in a selling campaign. Get it right and everything that follows — the price position, the buyer interest, the negotiation — has the best possible foundation. Get it wrong and the campaign spends its most valuable weeks recovering from a price position the market never supported.

The right appraisal is not the highest one. It is the one built from evidence — specific comparable sales, honest market context, a price position that generates genuine competition during the first 14 to 21 days when buyer attention is at its peak, and a timeline expectation that reflects the reality of your price bracket rather than the optimism of the agent who wants your listing.