Last Updated on February 13, 2026 by Andrew Mckiggan

Property Appraisal vs Valuation: What Is The Difference? (Australian Guide)

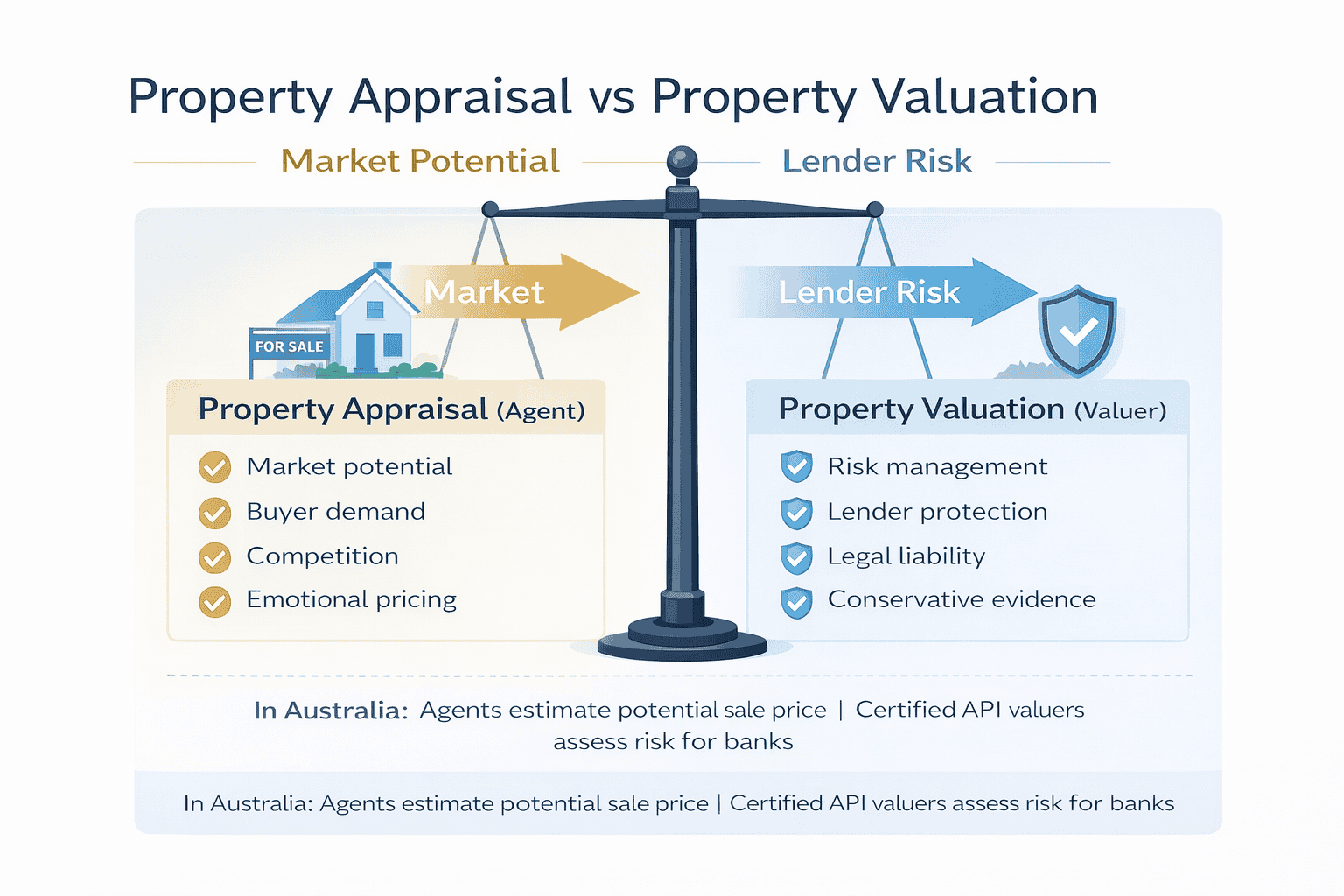

In the Australian real estate market, the main difference is that a Property Appraisal is an estimated market price provided by a real estate agent to guide a sale, whereas a Property Valuation is a legally binding report created by a qualified valuer for banking or court purposes.

⏱️ At A Glance: Key Differences

- Purpose: Appraisals are for selling; Valuations are for finance/legal.

- Cost: Appraisals are typically free; Valuations cost money.

- Legal Status: Banks require a formal valuation, not an appraisal.

Already know the difference?

If you are looking to sell and need an accurate market price, skip the reading and request your Free Property Appraisal here.

Analysis by Andrew McKiggan (Licensed RLA 248695) • Gawler East Real Estate

In the Australian property market, confusing a property appraisal with a property valuation can lead to costly misunderstandings — particularly during a sale, refinance, or purchase.

Although both aim to estimate a property’s value, they serve very different purposes, operate under different legal frameworks, and are prepared by professionals with different responsibilities.

Understanding the difference — and why the figures often don’t match — is essential when making decisions involving one of Australia’s largest financial assets.

Important Australian context:

The distinctions outlined in this article reflect Australian real estate law, lending requirements, and professional standards. Processes and terminology may differ significantly in other countries, including the United States and the United Kingdom.

1. Potential vs Protection (The Core Difference)

A property appraisal answers:

“What price could this property achieve in today’s market?”

It is forward-looking and focuses on buyer demand, competition, and marketing strategy.

A property valuation answers:

“What value can be relied upon for legal or financial purposes?”

It is conservative by design and exists to protect lenders, courts, insurers, and regulators.

Property Appraisal vs Property Valuation in Australia (Table of Key Differences)

| Aspect | Property Appraisal (Australia) | Property Valuation (Australia) |

|---|---|---|

| Primary Purpose | Estimate likely market price for selling | Risk management for legal and financial use |

| Who Conducts It | Licensed real estate agent | Certified Practising Valuer (CPV) |

| Focus | Market potential and buyer demand | Evidence-based, conservative assessment |

| Methodology | Comparable sales and local market knowledge | Direct comparison, summation, income capitalisation |

| Legal Standing | Not legally binding | Legally recognised document |

| Professional Liability | No legal liability for price outcome | Valuer is legally liable and insured |

| Bank Acceptance | Not accepted by Australian lenders | Mandatory for lending and refinancing |

| Inspection Type | May be visual or desk-based | Desktop, kerbside, or full internal inspection |

| Typical Cost | Often free | Usually paid ($300–$600+) |

| Best Used When | Planning to sell or test the market | Finance, legal, tax, or court requirements |

2. Market Sentiment vs Risk Management

Appraisals reflect market sentiment:

- Buyer emotion

- Scarcity

- Competition

- Timing

Valuations reflect risk management:

- Downside protection

- Evidence-based certainty

- Conservative assumptions

Both can be correct — they are simply solving different problems.

3. Legal Standing (Non-Binding vs Legally Recognised)

In Australia:

- Property appraisals are not legally binding

- Property valuations are legally recognised documents

An appraisal cannot be relied upon for lending, court proceedings, or statutory purposes. A valuation can.

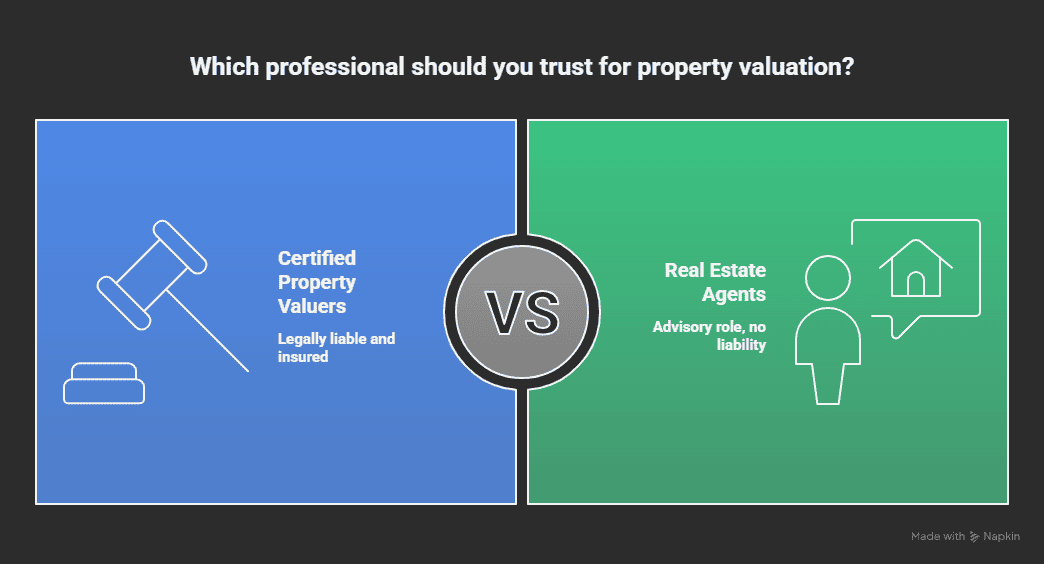

4. Professional Liability (Why Valuers Are Conservative)

This difference explains why valuations often come in lower.

Certified property valuers in Australia:

- Carry Professional Indemnity insurance

- Are legally liable for their valuation figures

- Can be held accountable if a lender suffers loss

Real estate agents do not carry price liability for appraisals.

Their role is advisory, not legally defensive.

This liability gap is a major reason valuations prioritise caution.

5. Methodology Used

Both agents and valuers consider comparable sales, but valuers are required to apply additional formal methodologies:

- Direct Comparison – Recent comparable sales

- Summation Method – Land value plus depreciated improvements

- Capitalisation of Income – For investment properties

Agents typically rely on direct comparison alone, as their role is pricing for market, not forensic assessment.

6. Desktop vs Physical Inspection Valuations (Modern Reality)

In 2026, many Australian lenders use:

- Automated Valuation Models (AVMs)

- Desktop valuations without physical inspections

These can sometimes produce conservative results.

Important practical note:

If a desktop valuation comes in low, homeowners may be able to request:

- A kerbside valuation, or

- A full internal inspection valuation

This can materially affect outcomes.

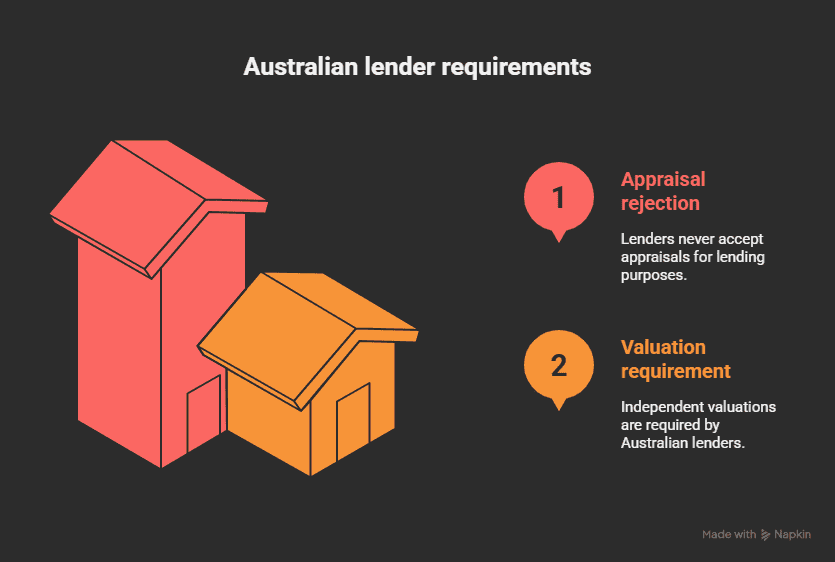

7. Bank and Lender Acceptance

Australian lenders:

- Never accept appraisals for lending

- Require independent valuations

Even if an appraisal is accurate, banks must rely on valuations for regulatory compliance and risk control.

8. The Real-World Consequence: The “Shortfall” Trap

A common scenario:

- Purchase price agreed: $900,000

- Bank valuation: $850,000

Result:

- Finance is assessed on $850,000

- The buyer must fund the $50,000 shortfall in cash

This is why “subject to finance” and “subject to valuation” clauses are critical protections in Australian contracts.

9. How to Prepare for Each (Practical Guidance)

Preparing for an Appraisal

Focus on emotional and lifestyle value:

- Presentation and styling

- Street appeal

- Highlighting suburb demand and amenities

Preparing for a Valuation

Focus on structural and documentary value:

- Approved building plans

- Renovation dates and costs

- Addressing visible defects or unapproved works

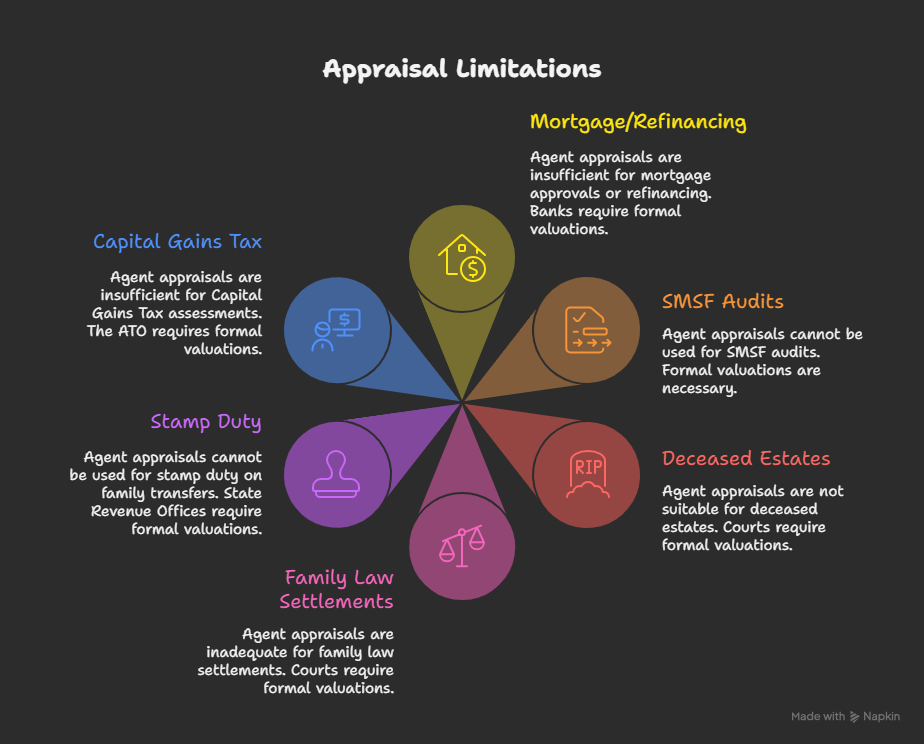

When a Valuation Is Mandatory in Australia

An agent’s appraisal cannot be used for:

- Mortgage approvals or refinancing

- SMSF audits

- Deceased estates

- Family law settlements

- Stamp duty on family transfers

- Capital Gains Tax assessments

In these cases, Australian banks, courts, the ATO, and State Revenue Offices require formal valuations.

Frequently Asked Questions For Property Appraisal vs Valuation (FAQs)

Can an appraisal and a valuation be the same figure?

Short Answer: Yes, but they are never legally interchangeable.

While a real estate agent (appraisal) and a certified valuer (valuation) might both estimate your home is worth $850,000, the documents serve different masters. The appraisal is a marketing tool to attract buyers, while the valuation is a risk document to protect a lender. A bank will never accept the agent’s figure, even if it matches the valuer’s figure exactly.

Why do Australian banks ignore real estate agent appraisals?

The Core Reason: Liability and Risk.

Real estate agents do not carry legal liability if a property sells for less than their appraisal. Certified Practising Valuers (CPVs), however, are legally liable for their assessment.

Regulatory Requirement: Australian banking regulations require lenders to use independent, insured professionals to assess the security of a mortgage. An agent has a vested interest in the sale; a valuer must remain independent.

Can I challenge a low bank valuation?

Yes, but you need hard evidence.

You cannot challenge a valuation simply because you disagree with the price. You must provide comparable sales evidence that the valuer missed or factual corrections (e.g., they listed it as 3 bedrooms when it has 4).

The Solution: Ask your lender for a “Check Valuation” or request a full internal inspection if the original was done via “Desktop” (remote) assessment.

Do renovations always increase the property valuation?

No. Cost does not equal Value.

Valuers assess “Contributory Value.” If you spend $50,000 on a swimming pool, it might only add $20,000 to the official valuation because pools limit the buyer pool.

Key Takeaway: Cosmetic renovations (paint, flooring, kitchens) generally offer a better return on valuation than structural changes or landscaping.

Which is more important when selling: The Appraisal or Valuation?

It depends on which stage of the sale you are in.

- For the Sale Price: The Appraisal is more important. It reflects what emotional buyers are willing to pay in competition.

- For the Contract Security: The Valuation is more important. If the valuation comes in low, the buyer’s finance may fall through, crashing the sale.

Are property appraisals free in Australia?

Yes, almost universally.

Most real estate agents provide property appraisals “gratis” (free of charge) as a way to introduce their services and demonstrate their local market knowledge.

Local Service: If you own property in Gawler, Willaston, or surrounding suburbs, Andrew McKiggan at Gawler East Real Estate offers comprehensive free appraisals that include recent sales data and a marketing strategy review.

Final Thoughts: Using Both Correctly

In Australia:

- A property appraisal shows what may be achievable

- A property valuation confirms what can be relied upon

Used together — and at the correct stage — they provide clarity, reduce risk, and prevent costly surprises.

For homeowners in Gawler and surrounding suburbs seeking an accurate understanding of current market conditions, Gawler East Real Estate offers complimentary, no-obligation property appraisals to help you make informed next steps with confidence.

For more information on certified valuers and the valuation process, visit the Australian Property Institute